The $54 trillion horizontal wealth transfer is coming for your family. Here’s what most couples aren’t doing to prepare.

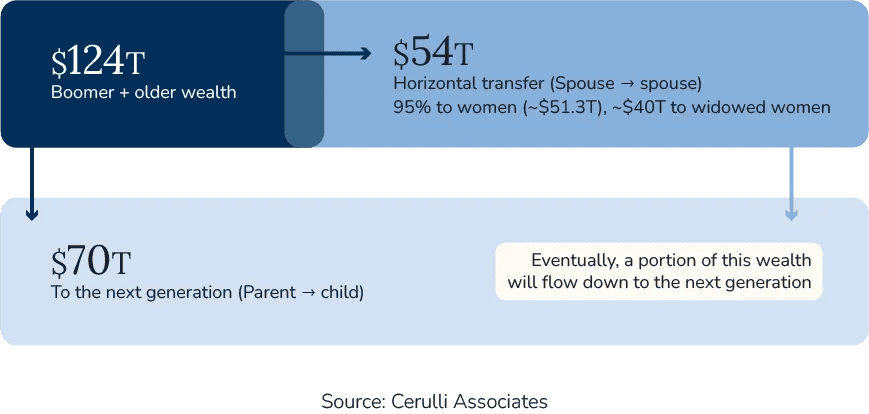

Everyone has heard of the Great Wealth Transfer. According to Cerulli Associates, an estimated $124 trillion in assets will change hands by 2048 as the Boomer generation passes its wealth to the next. It’s a staggering figure, and it dominates the conversation in financial planning, estate law, and family governance.

But there’s always another chapter to the story.

Before that money flows down, most of it will first flow sideways—from one spouse to another. Cerulli estimates that $54 trillion will pass between spouses in what researchers call the “horizontal transfer.” An estimated 95% of that will go to women, and roughly $40 trillion will go specifically to widowed women in aging cohorts.

For most families, the first great wealth event is a lateral move—and it receives surprisingly little coverage.

The survivor’s penalty: what changes the day after

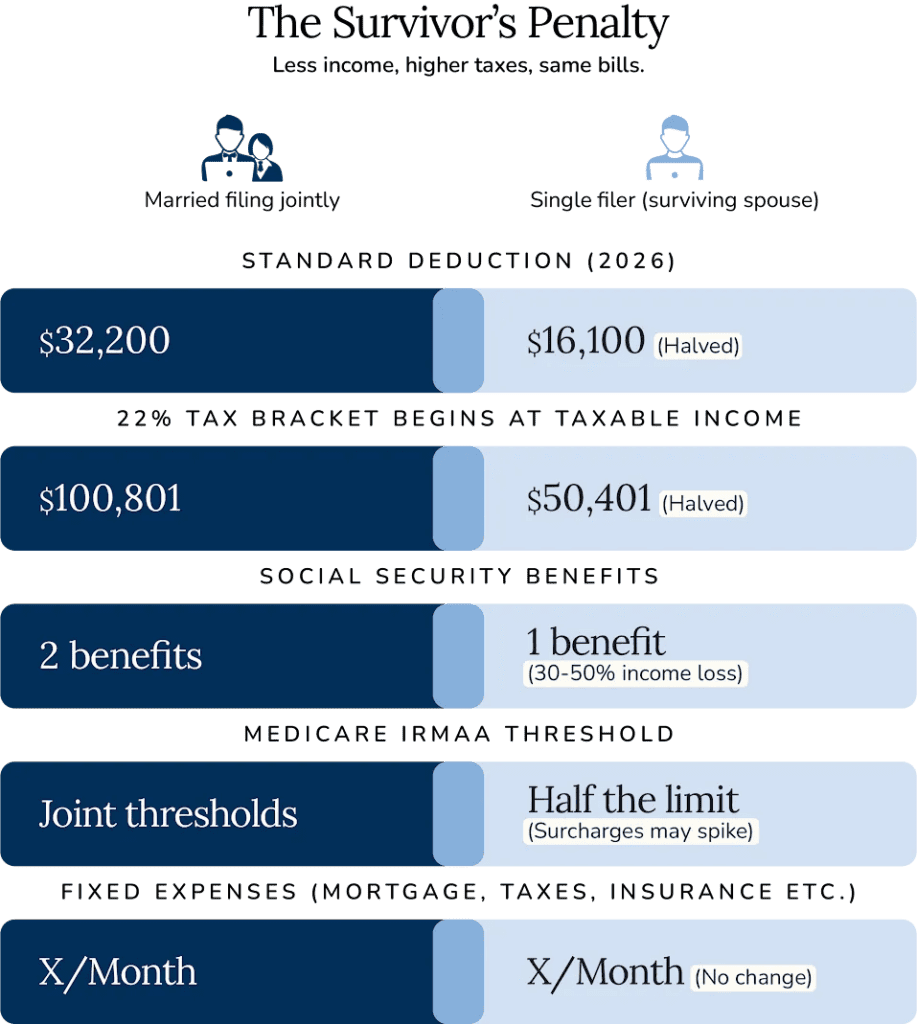

When a spouse dies, a cascade of financial changes begins—often within weeks—that can reshape a surviving spouse’s income, tax burden, and long-term financial picture. The compound effect of these changes is sometimes called the “survivor’s penalty,” and it catches even well-prepared families off guard.

Start with Social Security. A married couple typically receives two benefits; when one spouse dies, the smaller benefit disappears. The survivor keeps the larger of the two, but the household loses the other entirely. For couples where both spouses claimed benefits, this can mean a 30–50% reduction in Social Security income overnight.

Then come the taxes. A surviving spouse can file jointly for the year of the death, but after that, they become a single filer. In 2026, the standard deduction for married couples filing jointly is $32,200; for a single filer, it drops to $16,100—a reduction of $16,100. The tax brackets compress as well. A married couple doesn’t hit the 22% bracket until $100,801 in taxable income; a single filer reaches it at $50,401. The same income, taxed more heavily, in the hands of one person instead of two.

Medicare costs can spike, too. Income-Related Monthly Adjustment Amount (IRMAA) surcharges are based on modified adjusted gross income, and the thresholds for single filers are roughly half those for married couples. A surviving spouse who inherits a traditional IRA and begins taking required distributions may find their Medicare premiums jumping by hundreds of dollars per month.

Meanwhile, most fixed expenses—the mortgage, property taxes, homeowner’s insurance, utilities—don’t change at all. The house still costs the same to maintain. It just has to be maintained on less income, with a higher tax rate, by a person who may be making financial decisions through grief for the first time.

The numbers behind the gap

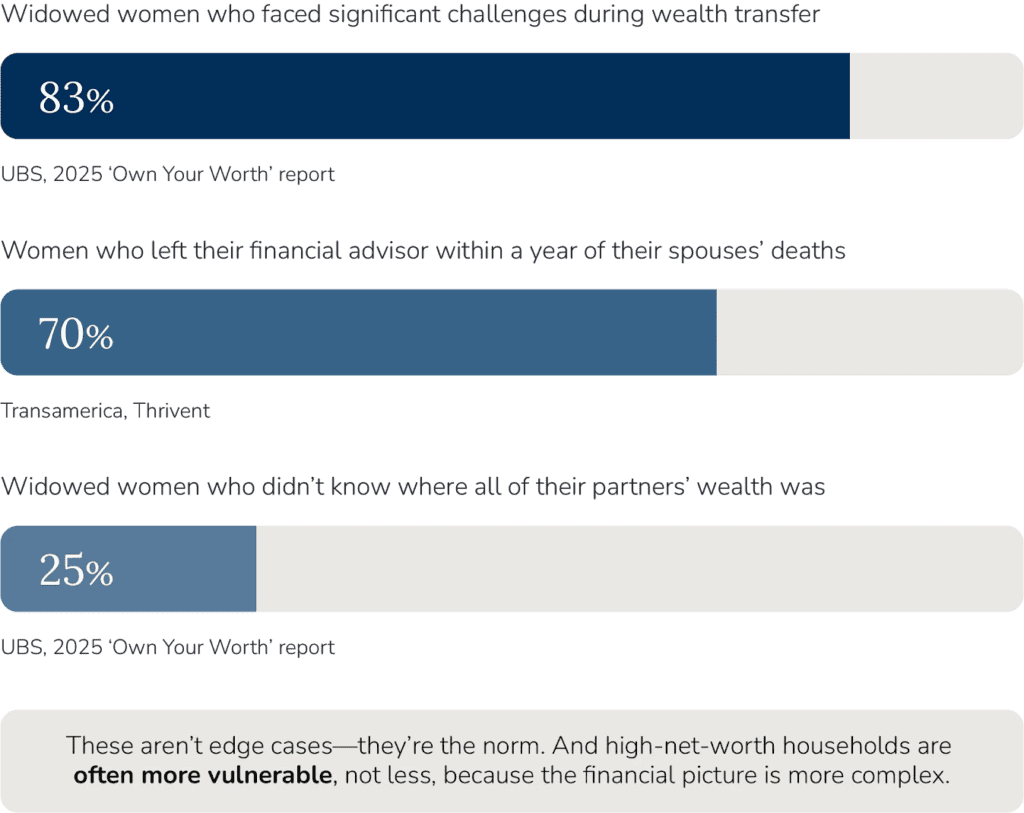

If the survivor’s penalty were only a tax problem, it would be manageable. But UBS’s 2025 Own Your Worth report paints a more troubling picture: 83% of recently widowed women reported facing significant challenges during the wealth transfer process, including financial surprises, the absence of a clear plan, and conflicts among heirs. One in four widowed women said they did not know where all their partner’s wealth was before he died.

These are not edge cases. They are becoming the norm and are not confined to families of modest means. High-net-worth households are often more vulnerable, not less, because the financial picture is more complex: multiple brokerage accounts, trusts, business interests, real estate in several states, concentrated stock positions, deferred compensation, and partnerships with intricate operating agreements.

Perhaps the most telling statistic comes from industry research cited by Thrivent: roughly 70% of women leave their financial advisor within the first year of their spouse’s death. The reasons vary—the relationship was with the deceased spouse, the advisor didn’t communicate well with both partners, the surviving spouse felt patronized or ignored—but the effect is the same. At the moment of greatest financial vulnerability, the surviving spouse is often starting over with no advisor, no plan, and no clear picture of what they own.

What the new tax law changes—and what it doesn’t

The One Big Beautiful Bill Act, signed into law in 2025, permanently raised the estate and gift tax exemption to $15 million per individual—$30 million for married couples—beginning January 1, 2026, with future inflation indexing. For most families, this is welcome news: the vast majority of spousal transfers will not trigger a federal estate tax. Portability of the unused exemption remains available, allowing a surviving spouse to use both their own exemption and their deceased spouse’s unused portion.

But there is a critical administrative step that is easily overlooked in the throes of bereavement: to elect portability, the surviving spouse must file IRS Form 706, even if no estate tax is owed. That small oversight—missing a single form during an incredibly demanding period—can evaporate a nine-figure exemption.

The OBBBA also introduced changes that affect charitable giving for surviving spouses. Beginning in 2026, a new 0.5% floor on adjusted gross income applies to charitable deductions for itemizers, and the value of itemized deductions is capped at 35% for top-bracket earners. For a surviving spouse who has historically relied on charitable giving as a key part of their tax strategy, these changes require a fresh look at the timing and structure of donations—ideally before the transfer happens, not after.

What the new law does not fix is the survivor’s penalty itself. The bracket compression, the loss of Social Security income, the IRMAA cliffs—all remain unchanged. The estate tax exemption addresses how much can transfer; it says nothing about what happens to the person who receives it.

5 things couples should do now

Conduct a survivor scenario.

Ask your advisor to model what happens to the surviving spouse’s income, taxes, Medicare costs, and overall cashflow if either spouse dies first—not just the wealthier one. The analysis should account for Social Security changes, bracket compression, IRMAA thresholds, and the shift in required minimum distributions. If your advisor has never run this scenario for you, it should be the first item on the agenda at your next review.

Ensure both spouses know where everything is.

This goes well beyond account numbers. Both partners should know who the financial advisors, attorneys, and CPAs are; where the estate documents are stored; what the access credentials are for online accounts; which assets are titled in whose name; what insurance policies exist and how to file a claim; and whether there are any business interests, partnership agreements, or deferred compensation arrangements that require action upon death.

Review trust language in light of the $15 million exemption.

Many estate plans were drafted when the federal exemption was $5 million or less. Formula clauses in those documents—provisions that automatically fund a bypass trust up to the exemption amount—may now direct far more money into irrevocable trusts than anyone intended. A trust that was designed to hold $5 million might now absorb $15 million, leaving the surviving spouse with restricted access to funds that were meant to support their lifestyle. An estate attorney should review and, if necessary, update these provisions.

Consider Roth conversions while both spouses are alive.

Converting traditional IRA assets to Roth accounts while a couple can still file jointly—and use the wider married-filing-jointly tax brackets—can meaningfully reduce the surviving spouse’s future tax burden. Once one spouse dies, the brackets compress, and conversions become more expensive. A phased conversion strategy over several years, ideally coordinated with your tax advisor, can smooth the tax impact and create a pool of tax-free income that the surviving spouse can draw on without triggering IRMAA surcharges or bracket creep.

Discuss the plan—out loud, together.

The UBS data makes one finding clear: the leading indicator of a smooth financial transition is whether both spouses were actively involved in financial planning conversations before the event. That means sitting down together with your advisor at least once a year, asking questions, and making sure the plan reflects what both of you need. Couples who do so spare the surviving spouse the added burden of navigating the unknown during a time that is already emotionally difficult—there’s no need to make it financially so, too.

The Conversation Worth Having

Of all the wealth transitions a family will face—retirement, a business sale, an inheritance, a cross-state move—the loss of a spouse is the one that often carries the most emotional weight and allows the least preparation time for the most significant adjustment period.

In moments like these, the best thing you can do for the person you love is make sure they are never forced to navigate a financial emergency on top of a personal one. That starts with a conversation—an honest, specific, unhurried conversation about what would happen, what would change, and what needs to be in place. It is, by any measure, one of the most important financial planning conversations a couple can have.

And ideally, it happens long before it’s needed—if it hasn’t yet, we’re here to help.

Promus Advisors, an SEC-registered investment adviser, is an affiliate of Bellwether Investment Management, Inc. (“Bellwether”). Promus Advisors provides fee-based asset management and advisory services. Bellwether and Promus Advisors have entered into arrangements in which Bellwether may refer clients with financial advisory needs to Promus Advisors. Please note that SEC registration does not constitute an endorsement of the firm by the Securities and Exchange Commission, nor does it indicate that the adviser has attained a particular level of skill. Promus Advisors and its investment adviser representatives are in compliance with the current filing requirements imposed upon SEC-registered investment advisers by those states in which Promus Advisors maintains clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any corresponding performance level(s), or be suitable for any specific client’s portfolio. Promus Advisors does not guarantee that any benchmark or indices used by Bellwether will match a given portfolio. Furthermore, asset allocation and/or diversification does not necessarily improve an investor’s performance or eliminate the risk of investment loss.