You spent decades putting money into your business. On closing day, the money comes back out. The question is whether it arrives with a plan, or just a balance—thankfully, how you approach this liquidity event can determine the answer and strengthen your overall wealth plan.

How liquidity events are showing up now

Global dealmaking has come back in force, with 2025 on track for about 4.8 trillion dollars in global M&A value, a roughly 36% increase from 2024 and the second-highest total on record. For many founders and business owners, that rebound shows up as unsolicited calls from buyers, term sheets arriving sooner than expected, and a growing sense that the timing of a sale may be set by the market as much as by personal preference.

At the same time, research suggests planning often lags opportunity. More than half of U.S. employer businesses are already owned by people 55 and older, yet a large share do not have a formal, documented succession or exit plan. That gap between transaction pressure and preparation is where “How much is enough?” becomes both a financial question and a family question.

Why “How much is enough?” can mislead

For many owners, the first instinct is to pick a single number: a sale price that feels large enough to make future decisions easy. In practice, that headline value says little about what the proceeds can support once taxes, ongoing expenses, healthcare costs, and market behavior are taken into account.

Focusing solely on a target valuation can also distract from other variables that matter just as much, such as how long the wealth needs to last, how much flexibility is needed, and whether there are specific commitments to children, employees, or causes.

There is also a planning gap on the personal side. Surveys show that while a high percentage of employer-business owners intend to sell or transfer their business, a meaningful minority still report having no clear plan for the transition, even as they approach traditional retirement age. Against that backdrop, treating “How much is enough?” as a quick mental benchmark can leave important questions unanswered about lifestyle, legacy, and resilience.

From business to family balance sheet

A sale, recapitalization, or major funding event generates liquidity—given that it’s often the end goal of building a business, this is well-known by most measures.

But we’d like to offer a different perspective. It effectively turns a single, illiquid operating company into a diversified family balance sheet. Where most of the net worth may once have been tied to enterprise value, cashflow, and a handful of key customer or supplier relationships, the post-transaction picture often includes a broader mix of cash, marketable securities, and, in some cases, new private investments.

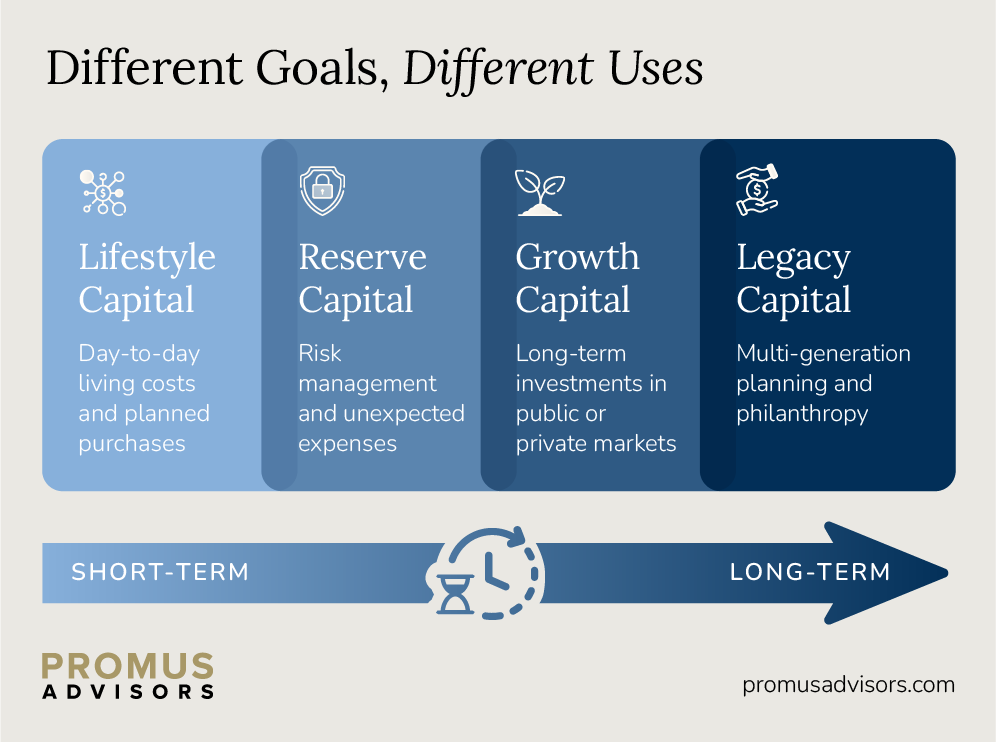

Thinking in terms of a family balance sheet can help bring structure to that shift. Proceeds can be mapped into distinct segments, such as:

Building a framework for “enough”

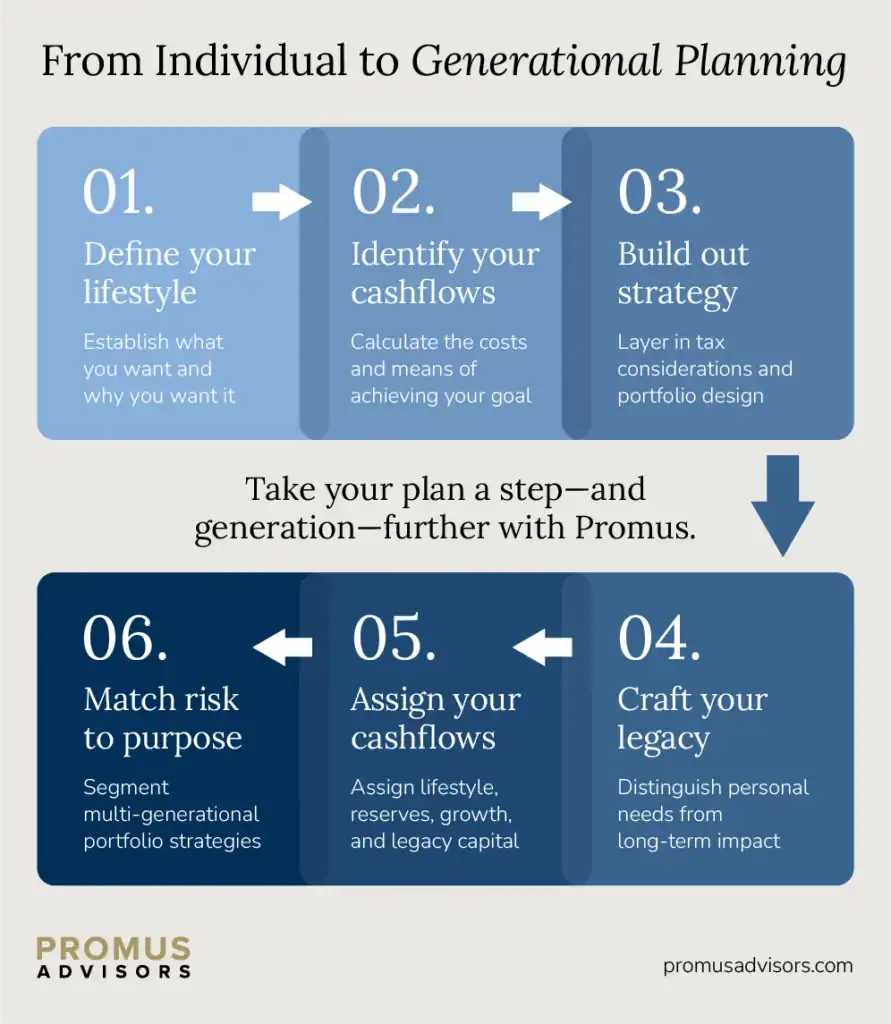

Instead of starting with a sale price, we’ve found that productive planning conversations begin with what the wealth is expected to enable or accomplish. A practical approach might include three steps: clarifying desired lifestyle, modeling cashflows, and incorporating taxes and investment assumptions. Clarifying lifestyle means translating broad preferences—travel, support for family members, potential relocation—into approximate annual spending figures, both now and later in life.

For one seller, “enough” might mean funding $400,000 of after‑tax spending each year for 30 years with a high degree of confidence; for another, it may mean a more modest lifestyle target but larger, recurring gifts to children or charities. Small changes in annual spending, the timing of big purchases, or how much is given away during life can meaningfully change the level of wealth required to sustain those choices.

From there, projected cash flows can be mapped over a multi-decade horizon, incorporating expected recurring expenses, healthcare, one-time costs, and reasonable assumptions about inflation and investment returns. Taxes are layered on at two levels: the initial cost of realizing the liquidity event and the ongoing tax profile of the resulting portfolio.

If anyone can appreciate contingency planning, it’s likely entrepreneurs. We’ve always found it useful to share a range of possibilities instead of a single outcome scenario, so clients can understand how spending or gifting decisions affect the probability that their portfolio will support their goals over time.

What often goes wrong after a liquidity event

Even with careful preparation, a major liquidity event can be disorienting. Wealth, at the end of the day, is a tool that provides optionality—if that sudden windfall isn’t accompanied by an idea of what to do with it, being flush with options can be overwhelming. This often translates to overspending shortly after the sale; relatively small recurring expenses can compound faster than anticipated when new habits form around a larger account value.

Another recurring pattern is replacing concentrated risk with a different concentration rather than with true diversification—for example, reallocating a large portion of the proceeds to a single new private deal, a narrow sector, or a small group of similar managers. Owners also sometimes underestimate how many personal and family expenses are being covered by the business, from healthcare to travel, which can raise the amount required to sustain their preferred lifestyle once those costs move onto the family balance sheet.

Legacy and the next generation

Estate planning is another consideration, and a deluge of ownership transition paperwork is likely the last thing on your mind. Delays in updating estate documents and beneficiary designations, even as wealth shifts into new accounts and entities, can complicate—rather than clarify—matters for future heirs.

Some of the most effective planning happens before a sale is signed. For owners whose projected proceeds would place them near or above the federal estate tax exemption—currently $15M per person and indexed to inflation—knowing how much capital is truly needed for their own lifetime spending can open the door to pre‑sale strategies. If a seller determines a certain amount is needed to support their lifestyle and expects to receive far more in total value, a portion of the excess can sometimes be transferred into trusts for children or grandchildren before the transaction, so that future appreciation occurs outside of the taxable estate.

Beyond tax efficiency, the core concept here is portfolio segmentation. Capital earmarked for second- or third-generation goals can be invested with a different time horizon and risk profile than assets needed to fund near-term spending, subject to a thoughtful asset allocation process and the family’s overall tolerance for risk.

When a liquidity event represents the culmination of decades of work, it often coincides with a broader conversation about what comes next for children and grandchildren. Planning the family balance sheet with that context in mind can help translate values into structures. Remember, those same values are the ones that brought you success in the first place—in many ways, they’re the true wealth to inherit, as they can help your children develop and maintain financial independence without whittling away at what you leave them.

Tools such as trusts and coordinated charitable strategies can serve several roles at once: managing taxes, providing clarity around decision-making, and creating opportunities to educate younger family members about stewardship and the responsibilities of wealth. Bringing adult children into parts of the planning process, where appropriate, can also help align expectations and reduce uncertainty about future responsibilities or expectations. For many families, this is where the idea of “enough” broadens from being a personal threshold to a multi‑generation framework.

Why coordination matters

The financial implications of selling a business, completing a recapitalization, or running a significant tender offer generally extend beyond any single professional discipline. At Promus, we organize a coordinated advisory team that typically includes a transactional attorney, tax advisor or CPA, estate planning counsel, and a fiduciary wealth advisor focused on portfolio construction and ongoing planning. Each brings a different lens to questions such as deal structure, timing, tax elections, and how the portfolio should be invested once proceeds are received.

Recent industry reports highlight that many private company leaders feel both an increased pressure to facilitate liquidity events and a lack of readiness around the details of executing them. Our team is here to model outcomes, stress-test assumptions, and align investment strategy with long-term objectives to help turn a single transaction into a financial trajectory that supports lifestyle, responsibilities, and legacy. For owners considering a sale or major liquidity event in the years ahead, the practical question is less about finding a perfect number and more about defining what the resulting wealth is expected to support, for whom, and for how long. When the money you built in your business comes back to you, having that plan in place allows it to show up as a well-structured family balance sheet rather than just a balance on a closing statement.

Promus Advisors, an SEC-registered investment adviser, is an affiliate of Bellwether Investment Management, Inc. (“Bellwether”). Promus Advisors provides fee-based asset management and advisory services. Bellwether and Promus Advisors have entered into arrangements in which Bellwether may refer clients with financial advisory needs to Promus Advisors. Please note that SEC registration does not constitute an endorsement of the firm by the Securities and Exchange Commission, nor does it indicate that the adviser has attained a particular level of skill. Promus Advisors and its investment adviser representatives are in compliance with the current filing requirements imposed upon SEC-registered investment advisers by those states in which Promus Advisors maintains clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any corresponding performance level(s), or be suitable for any specific client’s portfolio. Promus Advisors does not guarantee that any benchmark or indices used by Bellwether will match a given portfolio. Furthermore, asset allocation and/or diversification does not necessarily improve an investor’s performance or eliminate the risk of investment loss.