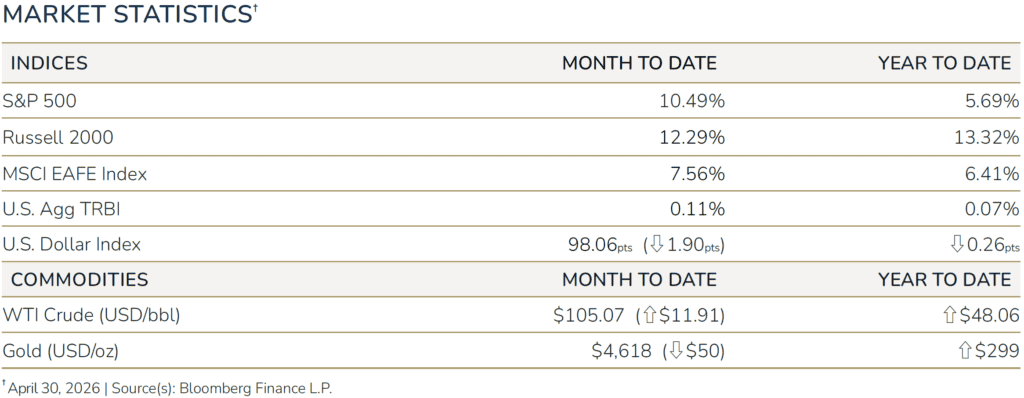

What the Rally Means—and What It Doesn’t

Despite a still-shuttered Strait of Hormuz causing a snag in global commodity trade, equity markets staged an impressive rebound in April.

The nations at war are technically bound by a ceasefire at the time of writing. But that agreement is fragile at best; progressing toward peace and backsliding into open conflict seem to trade headlines daily. The sudden shifts have led to intense volatility as investors recalibrate to the latest developments.

The ongoing crisis has shown that optimism is a more eager emotion than pessimism. Markets have been quick to rebound with any hint of de-escalation, and in general, the pullbacks have been less severe than historical precedents.

Perhaps it’s conviction, or perhaps it’s overly dismissive of risk—in either case, consumer spending has shown resilience so far. Fiscal support across North America has certainly helped, yet that buoy becomes progressively more difficult to maintain as time goes on. Government ledgers are stretched as they are.

The most immediate consequence of spiking oil prices is a drag on household spending—consumer prices rose 3.8% annually in April, marking the highest rate since May 2023. The next step would be companies passing along higher fuel-related costs to consumers. Third-order effects would be the decoupling of supply chains as commodities become stuck in transit. Each stage can contribute to a feedback loop of sorts.

Whether the event is disruptive or destructive is a function of time—the longer it persists, the wider the ripples. Central banks would typically forgive isolated energy pressures when making interest rate decisions, but the question is now one of transmission: how might temporary factors devolve into lasting inflation?On the equities side, we can look at duration and supply shocks in terms of prices and valuations. Price movements are short-term in nature, affecting levels without impeding underlying trends. Valuation shifts are structural—weaker earnings, compressed price-to-earnings multiples—and reconfigure overall market trajectory. For now, it appears to be relatively contained as energy-related inputs are repriced, not a systemic shift in valuations or growth outlooks.

Portfolio Outlook: Navigating an Uncertain Global Environment

From government treasuries to growth stocks, the near-term fate of markets is highly dependent on when the Strait of Hormuz reopens and global shipping normalizes.

Bond Markets and the Cost of Geopolitical Conflict

The cost of war is steep. Governments must fund military operations, and when the operations themselves jeopardize price stability at the household level, consumers indirectly share in the costs. On top of existing budget deficits and disappearing tariff revenues, it is not so surprising to see long-term yields climb and meager bond returns.

Iran’s influence abroad may run up against domestic changes too. Kevin Warsh has been confirmed as the next chair of the Federal Reserve. Although a vocal critic of restrictive policy and past committee decisions, he is only one vote among a variety of views and voices. The central bank, as a whole, will be keen to maintain its independence from political influence and its credibility in managing inflation.

AI Earnings Growth vs. Concentration Risk in U.S. Equities

Corporate earnings reports have been a bright spot, taking a particular shine to the technology sector, where spending on AI infrastructure continues to drive growth. And there may be room for further acceleration. Expectations have surprisingly risen since the war’s outset, with the consensus hoping to see profit growth in the high teens over the coming year. That may be difficult to achieve should the global crisis continue without a clear expiration date.

The renewed concentration in U.S. markets gives us pause. While AI’s underlying potential is immense, advancements are inherently difficult to forecast. As demonstrated in March, innovation comes on suddenly, and its nature is to displace. This is bound to create ongoing volatility, which necessitates prudence when weighing exposure to a single theme, especially when that theme is known and valued for transforming entire industries—often starting with itself.

Energy Supply Disruption and the Case for Infrastructure Diversification

Dozens of refineries, oil fields, gas plants, ports, and more have been taken offline across the Gulf region. The widespread supply disruption has clear implications for corporations and countries depending on the region’s chief exports.

Indirectly or otherwise, this geopolitical episode has shed light on how overreliance can create (infra)structural vulnerabilities. Several nations have made decisive moves to diversify or domesticate energy sources, with uranium and LNG deals being particularly popular. Critical minerals have also been featured in several deal frameworks. Whether damaged in the war, dated by today’s standards, or outright nonexistent, private capital will be in high demand to repair, modernize, or build infrastructure facilities around the world. It’s worth noting that geopolitical risk—whether through military or diplomacy—can hinder returns; they can also highlight the need for tactical diversification.

Promus Asset Management, LLC, doing business as Promus Advisors, is an investment adviser registered with the SEC. Promus Advisors only conducts business in jurisdictions where it is properly notice filed, or is exempted from such filing requirements. Registration is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability.

Content should not be viewed as personalized investment advice. All expressions of opinion reflect the judgment of the author on the date of publication and are subject to change. A professional advisor should be consulted before implementing any of the strategies discussed.

All investments and strategies have the potential for profit or loss. Index performance does not represent results obtained by Promus Advisors and does not reflect the impact that advisory fees and other expenses will have on the returns. There are no assurances that an investor’s portfolio will match or exceed any particular benchmark. Alternative investments are speculative, may be susceptible to fraud, involve a high level of risk, and may experience significant price volatility. You could lose all or a substantial part of your money, and your interest may be illiquid. They may involve complex tax structures and higher fees.

Historical performance returns for investment indexes and/or categories, usually do not deduct transaction and/or custodial charges or an advisory fee, which would decrease historical performance results. Asset allocation, rebalancing, and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses.