KEY MESSAGES FROM YOUR INVESTMENT TEAM

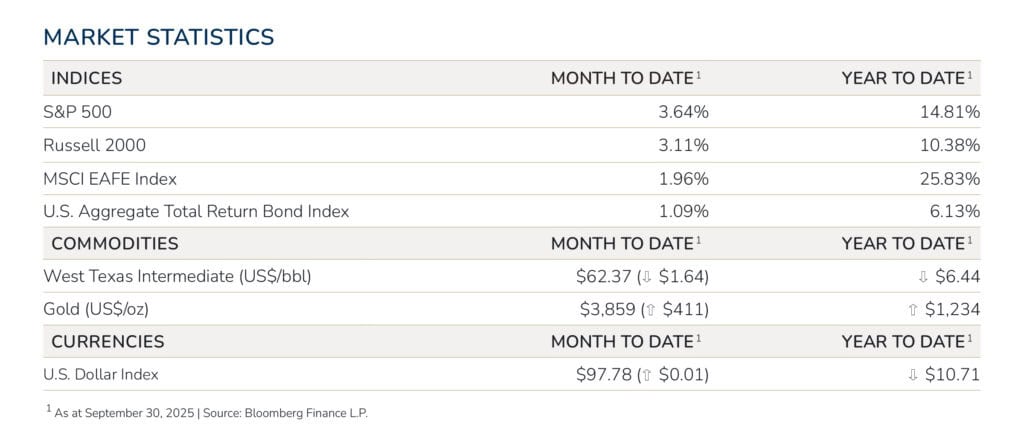

September rewarded investors with another exceptional month of equity returns. Many of the world’s leading stock indices marched higher despite what is historically a weak month of the year—a sound reminder that seasonal patterns shouldn’t be the basis for investment decisions.

The Federal Reserve delivered its first interest rate cut of 2025, reducing rates by 25 basis points to a range of 4.00%–4.25%. This long-awaited monetary easing paired well with technology’s continued momentum, driving heightened investor sentiment.

These combined forces are primarily responsible for market strength, so much so that valid concerns are largely being ignored. Underlying fundamentals show signs of weakening—particularly in labor markets—yet recently unlocked liquidity appears to be flowing into higher-risk assets rather than savings or less volatile securities.

Stability is lacking in other areas as well. At the time of writing, the federal government is shut down—ironically pausing much of the funding that caused the dispute in the first place: budgetary concerns.

The row between both major parties is likely a strategy to mobilize issues related to the debt ceiling in hopes of gaining political leverage ahead of the 2026 midterm elections. But they may come at a cost. If threats related to federal employment or dismantling entire departments and agencies become a reality, an already vulnerable labor market may suffer.

Yet investors are still largely unfazed. It is difficult to see a near-term trigger that could temper bullish sentiment, but equity markets are at their most expensive valuation ever along several key metrics.

From such heights, stock indices are susceptible to any downward reset on earnings expectations heading into 2026.

Outlook

Tariffs are contributing to inflation and hindering the economy. These are not ideal conditions. That said, declining interest rates are providing newfound liquidity around the world. Both forces are at

odds and could result in heightened volatility to close out 2025.

FIXED INCOME

Prior job creation data faced downward revisions, which gave the Federal Reserve enough leash to soften monetary policy and support the economy. The Federal Open Market Committee’s September meeting resulted in a 25-basis-point cut—the first of 2025—though there was one notable dissent from recently appointed Governor Stephen Miran, who favored a more aggressive policy action. The “dot plot” projections also revealed an internal debate over future policy moves, with FED officials split 10-9 on expectations for two more cuts before year-end. This division highlights the precarious position of the US central bank, caught between growing concerns about weakness in the labor market and rising inflationary pressures.

Fixed income—and many investments—hasn’t been able to keep pace with 2025’s highly concentrated equity markets. Those modest returns, however, provide additional value in the form of portfolio stability and predictable income. Avoiding losses, in many cases, can be just as valuable as securing gains. Municipal bonds may be particularly attractive for their respective tax advantages and present spread relative to U.S. Treasuries.

GLOBAL EQUITIES

The technology sector has driven much of the market’s gains, though September saw some profit-taking among mega-cap growth names—a natural occurrence when valuations reach historic levels. Interestingly, research from MSCI shows that value stocks have outperformed growth stocks outside of the U.S. year-to-date, signaling a potential change in investor sentiment. Closer to home, the continuing AI boom certainly has some similarity to the Dot-Com Era, but also some key differences. Unlike 1999–2001, today’s technology leaders are highly profitable with tremendous cashflow generation. Additionally, global interest rates are falling rather than rising, providing a more supportive backdrop for growth valuations.

Such conditions present challenges linked to risk management, capital appreciation, and expectations. There’s no true method of anticipating just how high markets can climb with any measure of certainty. As such, capitalizing on secular forces like AI means viewing it at the thematic level. Exposure can come in many forms, like opportunities in energy generation, computing power, or data storage. Taking profits along the way is often rewarding.

ALTERNATIVE INVESTMENTS

We’ve previously outlined how AI investments may be nearing an inflection point, and it warrants further discussion. Per McKinsey, a consulting firm, global data centers will require between $3.7 and $5.2 trillion to meet demand by 2030. While much of this will fall to hyperscalers, the sheer scale means alternative financing options will likely be called on—OpenAI’s $500 billion joint venture with Oracle and SoftBank and Meta’s $29 billion deal for the Hyperion data center, which included a $26 billion debt led by PIMCO, both come to mind.

The alternative investment landscape mirrors the broader market dynamic: enthusiasm for AI-related opportunities must be balanced against realistic timelines for implementation and return generation. Private markets typically lag public market volatility, which can provide stability during periods of uncertainty, but they’re not immune to fundamentals. As always, due diligence and patient capital remain essential. By the late 1990s, American telecom companies overestimated demand and laid over 80 million miles of fiber optic cables. Many failed to recover from the miscalculation, others like AT&T survived, adapted, and thrived. Selectivity is a valuable skill.

Promus Advisors, an SEC-registered investment adviser, is an affiliate of Bellwether Investment Management, Inc. (“Bellwether”). Promus Advisors provides fee-based asset management and advisory services. Bellwether and Promus Advisors have entered into arrangements in which Bellwether may refer clients with financial advisory needs to Promus Advisors. Please note that SEC registration does not constitute an endorsement of the firm by the Securities and Exchange Commission, nor does it indicate that the adviser has attained a particular level of skill. Promus Advisors and its investment adviser representatives are in compliance with the current filing requirements imposed upon SEC-registered investment advisers by those states in which Promus Advisors maintains clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any corresponding performance level(s), or be suitable for any specific client’s portfolio. Promus Advisors does not guarantee that any benchmark or indices used by Bellwether will match a given portfolio. Furthermore, asset allocation and/or diversification does not necessarily improve an investor’s performance or eliminate the risk of investment loss.